1

UNITED STATES DISTRICT COURT

FOR THE NORTHERN DISTRICT OF TEXAS

DALLAS DIVISION

UNITED STATES OF AMERICA,

Plaintiff,

v.

NEW WORLD AUTO IMPORTS, INC., a

corporation, also d/b/a Southwest Kia,

NEW WORLD AUTO IMPORTS OF

ROCKWALL, INC., a corporation,

also d/b/a Southwest Kia, and Southwest Kia of

Rockwall,

and

HAMPTON TWO AUTO CORPORATION, a

corporation, also d/b/a Southwest Kia, Southwest

Kia-NW, and Southwest Kia Mesquite,

Defendants.

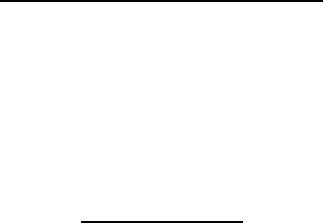

Case No.

COMPLAINT FOR CIVIL PENALTIES AND OTHER RELIEF

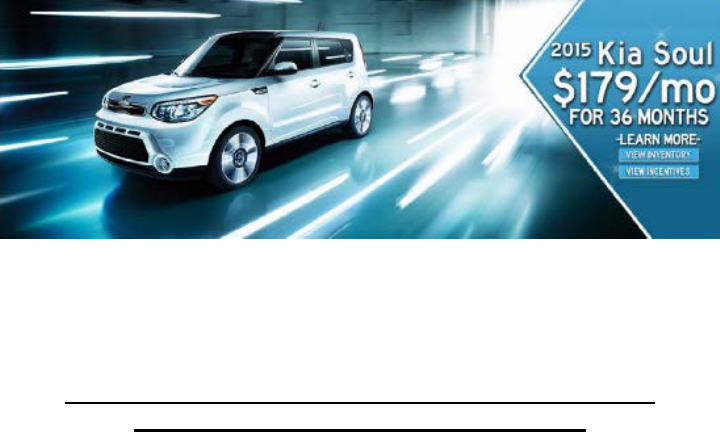

Plaintiff, the United States of America, acting upon the notification and authorization to

the Attorney General by the Federal Trade Commission (“FTC” or “Commission”), for its

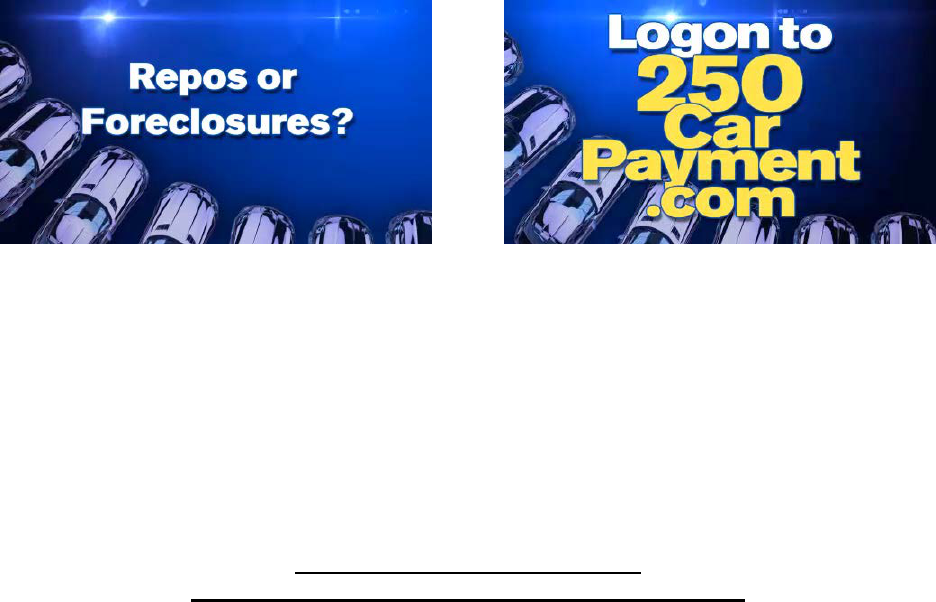

complaint alleges that:

1. Plaintiff brings this action under Sections 5(l) and 16(a) of the Federal Trade

Commission Act (“FTC Act”), 15 U.S.C. §§ 45(l) and 56(a), as amended; the Truth In Lending

Act (“TILA”), 15 U.S.C. §§ 1601-1667, as amended; and its implementing Regulation Z, 12

C.F.R. Part 226, as amended; the Consumer Leasing Act (“CLA”), 15 U.S.C. §§1667-1667f, as

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 1 of 23 PageID 1

2

amended; and its implementing Regulation M, 12 C.F.R. Part 213, as amended; to obtain

monetary civil penalties and other relief for Defendants’ violations of a final Commission order.

2. The jointly owned and operated Defendants are automobile dealers in the Dallas

metropolitan area. The Commission’s final order, effective May 30, 2014 (as to Hampton Two

Auto Corporation) and June 2, 2014 (as to the remaining Defendants), expressly requires

Defendants: (i) not to make misrepresentations about costs and terms of financing or leasing

vehicles; (ii) to conform their consumer credit advertisements to TILA and Regulation Z; (iii) to

conform their consumer lease advertisements to CLA and Regulation M; and (iv) to maintain

records related to representations covered by the final order. Defendants, from the effective date

of the order until February 2015, routinely violated these order provisions.

JURISDICTION AND VENUE

3. This Court has jurisdiction over this matter pursuant to 28 U.S.C. §§ 1331,

1337(a), 1345, and 1355, and 15 U.S.C. §§ 45(l), 56(a), and 1607(c).

4. Venue in this district is proper under 28 U.S.C. §§ 1391(b)-(d) and 1395(a).

DEFENDANTS

5. Defendant New World Auto Imports, Inc. (“Southwest Kia-Dallas”), also doing

business as Southwest Kia, is incorporated in the State of Texas. Its registered agent is located at

39650 Lyndon B. Johnson Fwy., Dallas, TX 75237, and its physical retail address is 39650

Lyndon B. Johnson Fwy., Dallas, TX 75237. At all times material to this complaint, Defendant

has participated in the acts and practices described in this complaint. Defendant transacts

business in this district, including through a motor vehicle retail store or lot, through television,

print, radio, Internet, email, and mobile device advertisements reaching consumers living in the

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 2 of 23 PageID 2

3

district, and through the websites southwestkia.com, southwestkia-dallas.com,

250carpayment.com, and DallasTruckWorld.com.

6. Defendant New World Auto Imports of Rockwall, Inc. (“Southwest Kia-

Rockwall”), also doing business as Southwest Kia and Southwest Kia of Rockwall, is

incorporated in the State of Texas. Its registered agent is located at 39650 Lyndon B. Johnson

Fwy., Dallas, TX 75237, and its physical retail address is 1790 East Interstate 30, Rockwall, TX

75087. At all times material to this complaint, Defendant has participated in the acts and

practices described in this complaint. Defendant transacts business in this district, including

through a motor vehicle retail store or lot, through television, print, radio, Internet, email, and

mobile device advertisements reaching consumers living in the district, and through the websites

southwestkia.com, southwestkia-rockwall.com, 250carpayment.com, and

DallasTruckWorld.com.

7. Defendant Hampton Two Auto Corporation (“Southwest Kia-Mesquite”), also

doing business as Southwest Kia and Southwest Kia of Mesquite, is incorporated in the State of

Texas. Its registered agent is located at 39650 Lyndon B. Johnson Fwy., Dallas, TX 75237, and

its physical retail address is 1919 Oates Dr., Mesquite, TX 75150. At all times material to this

complaint, Defendant has participated in the acts and practices described in this complaint.

Defendant transacts business in this district, including through a motor vehicle retail store or lot,

through television, print, radio, Internet, email, and mobile device advertisements reaching

consumers living in the district, and through the websites southwestkia.com, southwestkia-

mesquite.com, 250carpayment.com, and DallasTruckWorld.com.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 3 of 23 PageID 3

4

COMMERCE

8. At all times material to this complaint, Defendants have maintained a substantial

course of trade in or affecting commerce, as “commerce” is defined in Section 4 of the FTC Act,

15 U.S.C. § 44.

PRIOR COMMISSION PROCEEDING

9. In a Commission proceeding bearing Docket No. C-4437, the Commission

charged Defendants with, among other things:

i. Making false or misleading representations that, when a consumer

purchases a vehicle, the advertised monthly payments will pay off the

entire balance due on the car when in fact a large “balloon” payment

would be due at the end of the loan term, in violation of the FTC Act;

ii. Making false or misleading representations that, when a consumer leases

a vehicle, there would be almost no money due at lease signing when in

fact several fees amounting to hundreds or thousands of dollars would be

due at lease signing, in violation of the FTC Act;

iii. Disseminating consumer credit advertisements for vehicles that failed to

disclose and/or failed to disclose clearly and conspicuously terms for

financing the purchase of the advertised vehicles, in violation of

Regulation Z, 12 C.F.R. Part 226, as amended, and the Truth in Lending

Act (“TILA”), 15 U.S.C. §§ 1601-1667, as amended; and

iv. Disseminating consumer lease advertisements for vehicles that failed to

disclose and/or failed to disclose clearly and conspicuously terms for

leasing the advertised vehicles, in violation of Regulation M, 12 C.F.R.

Part 213, as amended, and the Consumer Leasing Act (“CLA”), 15

U.S.C. §§ 1667-1667f, as amended.

10. On February 20, 2014, the Commission issued its decision and order (“Consent

Order”) approving a settlement with Defendants. In pertinent part, Parts I, II, and III of the

Consent Order state:

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 4 of 23 PageID 4

5

I.

IT IS HEREBY ORDERED that [Defendants], directly or indirectly, in

connection with any advertisement for the purchase, financing, or leasing of

motor vehicles, shall not, in any manner, expressly or by implication:

A. Misrepresent the cost of:

1. Purchasing a vehicle with financing, including but not

necessarily limited to, the amount or percentage of the down

payment, the number of payments or period of repayment, the

amount of any payment, and the repayment obligation over the

full term of the loan, including any balloon payment; or

2. Leasing a vehicle, including but not necessarily limited to, the

total amount due at lease inception, the down payment, amount

down, acquisition fee, capitalized cost reduction, any other

amount required to be paid at lease inception, and the amounts

of all monthly or other periodic payments; or

B. Misrepresent any other material fact about the price, sale,

financing, or leasing of any vehicle.

II.

IT IS FURTHER ORDERED that [Defendants], directly or indirectly, in

connection with any advertisement for any extension of consumer credit, shall not

in any manner, expressly or by implication:

A. State the amount or percentage of any down payment, the number

of payments or period of repayment, the amount of any payment,

or the amount of any finance charge, without disclosing clearly and

conspicuously all of the following terms:

1. The amount or percentage of the down payment;

2. The terms of repayment; and

3. The annual percentage rate, using the term “annual

percentage rate” or the abbreviation “APR.” If the annual

percentage rate may be increased after consummation of

the credit transaction, that fact must also be disclosed; or

B. State a rate of finance charge without stating the rate as an “annual

percentage rate” or the abbreviation “APR,” using that term[.]

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 5 of 23 PageID 5

6

III.

IT IS FURTHER ORDERED that [Defendants], directly or indirectly, in

connection with any advertisement for any consumer lease, shall not, in any

manner, expressly or by implication:

A. State the amount of any payment or that any or no initial payment

is required at lease inception, without disclosing clearly and

conspicuously the following terms:

1. That the transaction advertised is a lease;

2. The total amount due at lease signing or delivery;

3. Whether or not a security deposit is required;

4. The number, amounts, and timing of scheduled payments;

and

5. That an extra charge may be imposed at the end of the lease

term in a lease in which the liability of the consumer at the

end of the lease term is based on the anticipated residual

value of the vehicle[.]

11. The Consent Order defines “clearly and conspicuously” to mean:

a. In a print advertisement, the disclosure shall be in a type size,

location, and in print that contrasts with the background against which it

appears, sufficient for an ordinary consumer to notice, read, and

comprehend it.

b. In an electronic medium, an audio disclosure shall be delivered in a

volume and cadence sufficient for an ordinary consumer to hear and

comprehend it. A video disclosure shall be of a size and shade and

appear on the screen for a duration and in a location sufficient for an

ordinary consumer to read and comprehend it.

c. In a television or video advertisement, an audio disclosure shall be

delivered in a volume and cadence sufficient for an ordinary consumer to

hear and comprehend it. A video disclosure shall be of a size and shade,

and appear on the screen for a duration, and in a location, sufficient for an

ordinary consumer to read and comprehend it.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 6 of 23 PageID 6

7

d. In a radio advertisement, the disclosure shall be delivered in a

volume and cadence sufficient for an ordinary consumer to hear and

comprehend it.

e. In all advertisements, the disclosure shall be in understandable

language and syntax. Nothing contrary to, inconsistent with, or in

mitigation of the disclosure shall be used in any advertisement or

promotion.

12. The Consent Order additionally states:

IV.

IT IS FURTHER ORDERED that [Defendants and their] successors and

assigns shall, for five (5) years after the last date of dissemination of any

representation covered by this order, maintain and upon request make available to

the Federal Trade Commission for inspection and copying: . . .

A. All advertisements and promotional materials containing the

representation; [and]

B. All materials that were relied upon in disseminating the

representation[.]

13. A copy of the Consent Order is attached hereto as Exhibit A. The FTC served the

Consent Order on Southwest Kia-Mesquite on or about May 30, 2014. The FTC served the

Consent Order on Southwest Kia-Dallas and Southwest Kia-Rockwall on or about June 2, 2014.

The Consent Order has remained in full effect since.

DEFENDANTS’ CONDUCT

14. Defendants’ three motor vehicle dealerships in the Dallas metropolitan area

operate under common ownership and management. In addition to three retail stores,

Defendants sell cars through several interconnected Internet websites. Defendants advertise their

dealerships and websites through a variety of media, including – but not limited to – television,

print, radio, Internet, email, and mobile device advertising targeting consumers in the Dallas,

Texas metropolitan area. Defendants often advertise jointly for all three dealerships, although

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 7 of 23 PageID 7

8

some advertising is Defendant specific. Through these dealerships, Defendants together sell or

lease more than 5,000 new and used vehicles per year.

Defendants’ Notice of the Consent Order

15. In 2014, all of the named Defendants stipulated to the Consent Order, specifically

acknowledging potential liability for “civil penalties in the amount provided by law and other

appropriate relief for each violation of the [Consent Order] after it becomes final.”

Advertisements with Hidden Conditions and Costs That

Misrepresent Terms of Financing or Leasing Vehicles

16. Since receiving service of the Consent Order, Defendants have offered to finance

or lease motor vehicles in thousands of television, print, radio, Internet, email, and mobile device

advertisements and on their various websites. These ads frequently misrepresented the

transaction by focusing only on a few attractive terms, such as a low monthly payment or annual

percentage rate, while concealing material terms that add significant extra costs or that limit who

can qualify for the advertised prices.

17. Defendants, for example, ran a joint television advertisement on local television

stations in July 2014.

1

A copy of this advertisement is attached as Exhibit B. They advertised

that consumers can “get up to $7,000 off New Kias in stock” when they purchase at a Southwest

Kia dealer. Defendants also offered “two vehicles for under $200 per month” both in the

voiceover and prominent text on the screen. Then, successive images of two vehicles

prominently advertised at a cost of $189 per month and $179 per month appear. Defendants only

mention in a barely legible, thirteen-line paragraph of dense, all caps, fine print flashed for two

seconds that the advertised terms are not for the sale of a vehicle, but rather for leases requiring a

$1,999 payment at lease signing. At no other time during the ad do Defendants disclose these

1

The comparative size of the images shown herein is similar to that which appears in advertisements provided to the

FTC by Defendants.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 8 of 23 PageID 8

9

terms. Across all media, from the effective date of the Consent Order until February 2015,

Defendants regularly used such disclosures and juxtaposition in a manner that tends to mislead

consumers.

18. Southwest Kia-Mesquite sent consumers direct mail advertisements for the

financing of new vehicles in October 2014. According to the prominent terms of the

advertisements, consumers could purchase a new vehicle for an attractive low monthly payment.

However, in almost illegible fine print far removed from the prominently advertised terms

Defendant Southwest Kia-Mesquite disclosed that consumers would be required to pay a down

payment and an enormous balloon payment of nearly half of the car’s suggested retail price at

the end of the financing term. For example, the mailer prominently advertised a 2015 Kia Rio

for sale for $179 per month.

Defendant Southwest Kia-Mesquite hid terms that raised the price. Only in the fine print –

illegible without magnification – could a consumer find the disclosure that $1,999 (plus tax, title,

and license fees) would be due upfront and $8,271 would be due at the end of the 38-month

financing term. A copy of this mailer, in the size produced to the FTC by Defendants, is

attached as Exhibit C. All three Defendants sent out substantively identical advertisements that

month, as well as others that were substantially similar.

19. Defendant Southwest Kia-Mesquite ran a Spanish-language television

advertisement on Dallas, Texas-area television stations. A copy of this advertisement is attached

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 9 of 23 PageID 9

10

as Exhibit D. The spoken and visual text of the commercial tells consumers that “por solo $500

de enganche puedes salir manejando” (“for only $500 down, you can leave driving”).

At no point in the commercial did Defendant Southwest Kia-Mesquite disclose any of the other

terms needed to allow consumers to comprehend the offer – e.g., required monthly payments and

the term for which payments must be made. Indeed, the advertisement never even clearly

explains whether the offer is for financing of a purchase or for a lease.

20. Defendants ran a banner advertisement on the Internet targeted toward consumers

in the Dallas, Texas metropolitan area that offered a vehicle for $179 per month for 36 months.

A copy of this advertisement, in the size produced to the FTC by Defendants, is attached as

Exhibit E. Nowhere in the visible portion of the banner advertisement did Defendants specify

whether the advertised price was for the sale or lease of the vehicle, or the required down

payment and APR (if a sale) or the total due at signing and whether a security deposit was

required (if a lease).

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 10 of 23 PageID 10

11

Defendants widely disseminated advertisements that failed to disclose clearly and conspicuously

material terms.

Advertisements with Hidden Limitations on the Ability of

Consumers to Qualify for Advertised Terms

21. Since receiving service of the Consent Order, Defendants have promoted motor

vehicles for lease or for sale on credit in advertisements which often featured attractive financing

terms or low monthly payments. In some instances, Defendants’ advertised terms often were

only available to a small subset of the consumers seeing the advertisement, and Defendants

failed to disclose clearly and conspicuously – if at all – the limitations on consumers’ ability to

qualify for the advantageous terms.

22. Defendants, for example, ran a television advertisement for the website

250carpayment.com on Dallas, Texas-area television stations in or around February 2015. A

copy of this advertisement is attached as Exhibit F. The advertisement begins with a voiceover

stating “Repos or foreclosures? 250carpayment.com can help,” accompanied by prominent text

encouraging consumers to log on to that website.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 11 of 23 PageID 11

12

After specifically seeking the attention of consumers with such credit issues, the commercial

advertises the availability of vehicles for $250 per month with a $250 down payment. In a fine

print disclosure it stated that these payments are based on a 4.25 annual percentage rate. In fact,

few if any borrowers with issues as severe as a reposession or foreclosure could have qualified

for that annual percentage rate.

Consumer Credit Advertisements

Without Required Clear and Conspicuous Disclosures

23. Since receiving service of the Consent Order, Defendants have promoted the

extension of consumer credit for motor vehicles, in thousands of television, print, radio, Internet,

email, and mobile device advertisements and at the various websites under their control.

Defendants’ credit offers often contain a prominent “triggering term” (as it is commonly known

under the Truth in Lending Act (“TILA”) and Regulation Z), requiring clear and conspicuous

disclosure of specific cost, annual percentage rate, duration, and down payment terms relating to

the transaction. From the effective date of the Consent Order until February 2015, many of

Defendants’ advertisements prominently advertised the amount of any down payment, the

number of payments or period of repayment, or the amount of any payment (“triggering terms”),

but failed to disclose, or clearly and conspicuously disclose, the full terms of repayment and the

annual percentage rate.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 12 of 23 PageID 12

13

24. Defendants, for example, ran an advertisement for used cars sold on credit on

Dallas, Texas-area television stations. A copy of this advertisement is attached as Exhibit G.

The commercial prominently states that there are 250 cars available with a $250 down payment

for $250 per month. White fine print at the bottom of the screen appears for about two seconds

against a grey background — making it effectively illegible — disclosing the remaining terms of

repayment and the finance charge expressed as an annual percentage rate. From the effective

date of the Consent Order until February 2015, Defendants widely disseminated advertisements

with fine print, difficult to read disclosures about finance terms.

25. Defendants ran an advertisement with a credit offer on Dallas, Texas-area

television stations in or around January 2015. The commercial offered new vehicles with

financing at a 0% rate for a financing term of sixty months. A copy of this advertisement is

attached as Exhibit H. The advertisement contains the duration of the financing contract (the

TILA “triggering term”) but fails to disclose the finance charge as an annual percentage rate.

Such omissions were common throughout many of Defendants’ advertisements for the sale of

motor vehicles with financing.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 13 of 23 PageID 13

14

Consumer Lease Advertisements Without

Required Clear and Conspicuous Disclosures

26. Since receiving service of the Consent Order, Defendants have promoted the

extension of consumer leases for motor vehicles in hundreds of television, radio, direct mail,

Internet, email, and mobile device advertisements and at the various websites under their control.

Defendants’ lease offers often contain a prominent “triggering term,” (as it is commonly known

under the Consumer Leasing Act (“CLA”) and Regulation M), requiring the clear and

conspicuous disclosure of specific terms relating to the transaction. From the effective date of

the Consent Order until February 2015, several of Defendants’ advertisements prominently

advertised the amount of a payment (a CLA “triggering term”), but failed to disclose, or clearly

and conspicuously disclose, that the transaction is a lease, the total amount due at signing or

delivery, or whether a security deposit is required.

27. In a July 2014 commercial, Defendants’ General Manager claims that consumers

can get two vehicles “for under $200 per month,” including a 2014 Optima for “$189/mo.” At

no point did Defendants state in the large text or the spoken script that the advertised monthly

payments were not for the sale of vehicles, but rather for leases bearing $1,999 down payments.

See Exhibit B. The advertisement contains the amount of the monthly payments (a CLA

“triggering term”). However, the advertisement only includes the following required disclosures

in the midst of a large block of fine print twelve lines long in difficult-to-read all caps white

lettering: (1) that the advertisement is for a lease; (2) the full amount due at lease signing; (3) the

number of payments; and (4) whether there is a security deposit. From the effective date of the

Consent Order until February 2015, Defendants widely disseminated several advertisements

which failed to disclose clearly and conspicuously necessary finance terms required by CLA.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 14 of 23 PageID 14

15

28. Defendants ran an Internet advertisement targeting consumers in the Dallas

metropolitan area that prominently offered a vehicle for “$219/mo for 36 months.” Although the

advertised price was for a lease, that fact was only clear if consumers read the fine print – which

would require significant magnification to do. Similarly, the consumer would have to look in the

fine print to learn that nearly $3,000 (the exact amount is not legible) would be due at lease

signing. A copy of the internet advertisement, in the size produced to the FTC by Defendants, is

attached as Exhibit I. The advertisement contains the CLA/Regulation M “triggering term” of

the amount of monthly payments. The following terms appear in the midst of the miniscule, fine

print seven lines long in difficult to read white lettering against a grey background: (a) that the

transaction was a lease, (b) the full amount due at lease signing, and (c) whether a security

deposit would be required. Defendants widely disseminated advertisements like these.

Consumer Credit or Lease Advertisements Without

Required Clear and Conspicuous Disclosures

29. Since receiving service of the final Order, Defendants have promoted their

business by running advertisements across a variety of media. Many of these offers are for the

sale of a vehicle with financing, while others are for the lease of a vehicle. In several instances,

Defendants’ advertisements contain offers that highlight one or two terms of a transaction, but

fail to disclose at any time whether the terms relate to the sale or lease of a vehicle or other

required cost disclosures.

30. Defendants, for example, ran an advertisement in Spanish, telling consumers “for

only $500 down, you can leave driving.” The commercial includes the amount down (a CLA

and a TILA “triggering term”) but never indicates whether the advertised terms are for financing

or a lease, and never provides the required cost disclosures. See Exhibit D.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 15 of 23 PageID 15

16

If the commercial is for a sale with financing, it fails to disclose: (a) the terms of repayment

including the number, amount, and timing of payments and (b) the finance charge expressed as

an annual percentage rate. If the commercial is for a lease, it fails to disclose: (a) that the

transaction is a lease; (b) the number, amount, and timing of payments; (c) a statement of

whether there is a security deposit; and (d) a statement that an extra charge may be imposed at

the end of the lease term, where the lessee’s liability is based on the difference between the

residual value of the leased property and the realized value.

31. Defendants’ Internet advertisement offered a vehicle for $179 per month for 36

months (“triggering terms”) without specifying whether the advertised price was for the sale or

lease of the vehicle.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 16 of 23 PageID 16

17

See Exhibit E. If the advertisement is for a sale with financing, it fails to disclose: (a) down

payment and (b) the rate of finance charge expressed as an annual percentage rate. If the offer is

for a lease, it fails to disclose: (a) that the transaction is a lease; (b) the amount due at lease

signing; (c) a statement of whether there is a security deposit; and (d) a statement that an extra

charge may be imposed at the end of the lease term, where the lessee’s liability is based on the

difference between the residual value of the leased property and the realized value. From the

effective date of the Consent Order until February 2015, Defendants widely disseminated

advertisements that failed to disclose clearly and conspicuously necessary cost terms required by

TILA and/or CLA.

Defendants’ Recordkeeping Failures

32. Defendants agreed, in Parts IV and VII of the Consent Order, to retain certain

business records, produce them upon request, and submit compliance reports. After the Consent

Order became effective, however, Defendants have failed to produce sufficient records. In

absence of these records, it is often impossible to gauge the degree of the Defendants’

compliance with the other provisions of the Order.

33. In their September 26, 2014 compliance report, Defendants stated that “With

respect to advertisements on Southwest Kia’s website and the internet, [Defendants are] in the

process of establishing a method to record and maintain such records and, once established, will

maintain such records for at least five (5) years from dissemination.”

34. In 2014 and 2015, FTC staff sought further compliance information pursuant to

the Consent Order from Defendants via narrowly tailored requests. Staff requested, among other

things, copies of Defendants’ mobile and Internet advertisements.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 17 of 23 PageID 17

18

35. In various productions in 2014 and 2015, Defendants produced screenshots of

mobile and Internet banner advertisements but were unable to provide either: (a) copies of the

advertisements in their native format or (b) copies of the advertisements in any other format that

would show all disclaimers, qualifications, or other information that consumers could view by

interacting with the banner using their cursor. For example, Defendants produced a banner

advertisement that included buttons for consumers to “view inventory” or “view incentives” but

could not or did not produce a version that could show those disclaimers.

See Exhibit E.

VIOLATIONS OF CONSENT ORDER

FIRST CAUSE OF ACTION

(CONSENT ORDER PART I – MISREPRESENTATIONS)

36. In numerous instances, from the effective date of the Consent Order until

February 2015, Defendants disseminated or caused the dissemination of advertisements

containing material facts regarding the cost or terms of offers for financing or leasing a motor

vehicle, that represented expressly or by implication:

A. The prominent costs or terms are inclusive of all material costs and terms

of the transaction;

B. The prominent costs or terms are generally available to consumers

targeted by the advertisements; or

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 18 of 23 PageID 18

19

C. The prominent costs or terms are for vehicle purchases, not leases.

37. In truth and in fact:

A. The prominent costs or terms do not include costs and terms such as large

down payments, balloon payments, capital cost reductions, acquisition fees, or other up-

front payments;

B. The prominent costs or terms are not generally available to consumers

targeted by the advertisement; or

C. The prominent costs and terms are for vehicle leases, and not purchases.

38. Defendants’ representations described in Paragraph 36 above, constitute

misrepresentations, in violation of Parts I(A) and (B) of the Consent Order.

SECOND CAUSE OF ACTION

(CONSENT ORDER PART II – TILA / REGULATION Z – CONSUMER CREDIT)

39. In numerous instances, Defendants disseminated or caused the dissemination of

offers promoting, directly or indirectly, the extension of consumer credit for a motor vehicle.

40. In numerous instances, from the effective date of the Consent Order until

February 2015, the offers for the extension of consumer credit for vehicles described in

Paragraph 39 stated the amount or percentage of any down payment, the number of payments or

period of repayment, the amount of any payment, or the amount of any finance charge, but:

A. Omitted the amount or percentage of the down payment or the terms of

repayment; or

B. Failed to state all required disclosures “clearly and conspicuously,” as

defined in the Consent Order, including the amount or percentage of the down payment

or the terms of repayment. These disclosures were not stated “clearly and

conspicuously,” because, among other deficiencies, they appeared in small type, in a

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 19 of 23 PageID 19

20

distant location, for a short duration, in a fast speed or cadence, in unintelligible language

or syntax, or were accompanied by distracting sounds or images.

41. By failing to make these disclosures required by Part II(A) of the Consent Order,

or failing to make the required disclosures “clearly and conspicuously,” Defendants violated Part

II(A) of the Consent Order.

42. In numerous instances, from the effective date of the Consent Order until

February 2015, the offers for the extension of consumer credit for vehicles described in

Paragraph 39 stated a finance charge, but failed to state the finance charge as an annual

percentage rate or APR, using those terms.

43. Defendants’ failure to make these statements required by Part II(B) of the Consent

Order constitutes a violation of Part II(B) of the Consent Order.

THIRD CAUSE OF ACTION

(CONSENT ORDER PART III – CLA / REGULATION M – CONSUMER LEASES)

44. In numerous instances, Defendants disseminated or caused the dissemination of

offers promoting, directly or indirectly, consumer leases for a motor vehicle.

45. In numerous instances, from the effective date of the Consent Order until

February 2015, the offers for consumer leases for vehicles described in Paragraph 44 stated the

amount of any payment or that any or no initial payment was required at lease inception, but:

A. Omitted a statement that the transaction advertised is a lease, the total

amount due at lease signing or delivery, a statement of whether or not a security deposit

is required, or the number, amounts, and timing of scheduled payments; or

B. Failed to state all required disclosures “clearly and conspicuously,”

as defined in the Consent Order, including a statement that the transaction

advertised is a lease, the total amount due at lease signing or delivery, a statement

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 20 of 23 PageID 20

21

of whether or not a security deposit is required, or the number, amounts, and

timing of scheduled payments. These disclosures were not stated “clearly and

conspicuously,” because, among other deficiencies, they appeared in small type,

in a distant location, for a short duration, in a fast speed or cadence, in

unintelligible language or syntax, or were accompanied by distracting sounds

or images.

46. By failing to make these disclosures required by Part III(A) of the Consent Order,

or failing to make the required disclosures “clearly and conspicuously,” Defendants violated Part

III(A) of the Consent Order.

FOURTH CAUSE OF ACTION

(CONSENT ORDER PART IV – FAILURE TO RETAIN AND PRODUCE RECORDS)

47. Part IV(A) of the Consent Order requires Defendants “for five (5) years after the

last date of dissemination of any representation covered by [the Consent Order], [to] maintain

and upon request make available to the Federal Trade Commission for inspection and

copying . . . all advertisements and promotional materials containing the representation.”

48. From the effective date of the Consent Order until February 2015, in numerous

instances in which Defendants disseminated specific offers to provide consumer credit or leases

in connection with motor vehicles, Defendants:

A. Did not maintain materials, such as complete copies of all advertisements

produced by or on behalf of Defendants, or

B. Did not make them available, upon request, to the FTC for inspection and

copying.

49. Defendants’ acts or practices, as described in Paragraph 48 above, violated Part

IV(A) of the Consent Order.

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 21 of 23 PageID 21

22

CIVIL PENALTIES

50. Each representation Defendants have made in violation of the Consent Order

constitutes a separate violation for which Plaintiff may seek civil penalties. Additionally, each of

Defendants’ failures to maintain and make available materials and its failure to submit true and

accurate written reports constitutes a separate violation for which Plaintiff may seek civil

penalties.

51. Each day Defendants have made, or have continued to make, representations in

violation of the Consent Order constitutes a separate violation for which Plaintiff may seek civil

penalties.

52. Section 5(l) of the FTC Act, 15 U.S.C. § 45(l), as modified by the Federal Civil

Penalties Inflation Adjustment Act of 1990, 28 U.S.C. § 2461 (note), and Section 1.98(c) of the

FTC’s Rules of Practice, 16 C.F.R. § 1.98(c), authorizes the Court to award monetary civil

penalties of up to $16,000 for each such violation of the Consent Order.

53. Under Section 5(l) of the FTC Act, 15 U.S.C. § 45(l), this Court is authorized to

permanently enjoin Defendants from violating the Consent Order and grant ancillary relief.

PRAYER FOR RELIEF

54. WHEREFORE, Plaintiff requests this Court, pursuant to 15 U.S.C. § 45(l), and

pursuant to the Court’s own equitable powers, to:

(1) Enter judgment against Defendants and in favor of the Plaintiff for each

violation alleged in this complaint;

(2) Award Plaintiff monetary civil penalties from Defendants for each violation

of the Consent Order alleged in this complaint;

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 22 of 23 PageID 22

23

(3) Enter a permanent injunction to prevent Defendants from violating the

Consent Order;

(4) Award Plaintiff its costs and attorneys’ fees incurred in connection with this

action; and

(5) Award Plaintiff such additional relief as the Court may deem just and proper.

DATED:

FOR THE COMMISSION:

JAMES A. KOHM

Associate Director for Enforcement

FRANK M. GORMAN

Assistant Director for Enforcement

_____________________________

MICHELLE SCHAEFER

COLIN D. A. MACDONALD

Federal Trade Commission

Division of Enforcement

600 Pennsylvania Avenue, NW,

Mail Drop CC-9528

Washington, DC 20580

(202) 326-3515, mschaefer@ftc.gov

(202) 326-3192, [email protected]

(202) 326-3197 (fax)

FOR THE PLAINTIFF

UNITED STATES OF AMERICA:

BENJAMIN C. MIZER

Principal Deputy Assistant Attorney

General, Civil Division

United States Department of Justice

JONATHAN F. OLIN

Deputy Assistant Attorney General

MICHAEL S. BLUME

Director

Consumer Protection Branch

ANDREW E. CLARK

Assistant Director

________________________

Jacqueline Blaesi-Freed

Trial Attorney

Consumer Protection Branch

U.S. Department of Justice

P.O. Box 386

Washington, DC 20044

Phone: (202) 353-2809

Fax: (202) 514-8742

Email: jacqueline.m.blaesi-

Case 3:16-cv-02401-K Document 1 Filed 08/18/16 Page 23 of 23 PageID 23