Investor

Presentation

March 2024

The Baylor Scott & White Charles A Sammons Cancer Center

Dallas, Texas

Disclaimers

This Healthpeak Properties, Inc. (the presentation is solely for your information,

is subject to change and speaks only as of the date hereof. This presentation is not complete

and is only a summary of the more detailed information included elsewhere, including in our

Securities and Exchange Commission filings. No representation or warranty,

express or implied, is made and you should not place undue reliance on the accuracy,

fairness or completeness of the information presented.

Forward-Looking Statements

Statements contained in this presentation that are not historical facts are "forward-looking

statements" within the meaning of Section 27A of the Securities Act of 1933, as amended,

and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking

statements include, among other things, statements regarding our and our intent,

belief or expectation as identified by the use of words such as

and other comparable and derivative terms or the

negatives thereof.

Examples of forward-looking statements include, among other things, (i) statements

regarding timing, outcomes and other details relating to current, pending or contemplated

acquisitions, dispositions, transitions, developments, redevelopments, densifications, joint

venture transactions, leasing activity and commitments, capital recycling plans, financing

activities, or other transactions; (ii) development and densification opportunities; (iii) outlooks

related to outpatient medical, lab, and CCRCs; and (iv) potential capital sources and uses.

You should not place undue reliance on these forward-looking statements. Pending

acquisitions, dispositions, joint venture transactions, leasing activity, and financing activity,

including those that are subject to binding agreements, remain subject to closing conditions

and may not be completed within the anticipated timeframes or at all. Forward-looking

statements reflect our current expectations and views about future events and are subject to

risks and uncertainties that could significantly affect our future financial condition and results

of operations. While forward-looking statements reflect our good faith belief and assumptions

we believe to be reasonable based upon current information, we can give no assurance that

our expectations or forecasts will be attained. Further, we cannot guarantee the accuracy of

any such forward-looking statement contained in this presentation, and such forward-looking

statements are subject to known and unknown risks and uncertainties that are difficult to

predict. These risks and uncertainties include, but are not limited to: macroeconomic trends,

including inflation, interest rates, labor costs, and unemployment; risks associated with the

merger transactions with Physicians Realty Trust (the including, but not limited

to, potential loss or disruption of current and prospective commercial relationships due to the

uncertainties about the Mergers, and the outcome of legal proceedings instituted against us,

our Board of Directors, and others related to the Mergers; our ability to integrate the

operations of the Company and Physicians Realty Trust successfully and realize the

anticipated synergies and other benefits of the Mergers or do so within the anticipated time

frame; changes within the industries in which we operate; significant regulation, funding

requirements, and uncertainty faced by our lab tenants; factors adversely affecting our

or ability to meet their financial and other contractual

obligations to us; the insolvency or bankruptcy of one or more of our major tenants,

operators, or borrowers; our concentration of real estate investments in the healthcare

property sector, which makes us more vulnerable to a downturn in a specific sector than if

we invested across multiple sectors; the illiquidity of real estate investments; our ability to

identify and secure new or replacement tenants and operators; our property development,

redevelopment, and tenant improvement risks, including project abandonments, project

delays, and lower profits than expected; the ability of the hospitals on whose campuses our

outpatient medical buildings are located and their affiliated healthcare systems to remain

competitive or financially viable; our ability to develop, maintain, or expand hospital and

health system client relationships; operational risks associated with third party management

contracts, including the additional regulation and liabilities of our properties operated through

RIDEA structures; economic conditions, natural disasters, weather, and other conditions that

negatively affect geographic areas where we have concentrated investments; uninsured or

underinsured losses, which could result in significant losses and/or performance declines by

us or our tenants and operators; our investments in joint ventures and unconsolidated

entities, including our lack of sole decision making authority and our reliance on our

financial condition and continued cooperation; our use of fixed rent escalators, contingent

rent provisions, and/or rent escalators based on the Consumer Price Index; competition for

suitable healthcare properties to grow our investment portfolio; our ability to foreclose or

exercise rights on collateral securing our real estate-related loans; any requirement that we

recognize reserves, allowances, credit losses, or impairment charges; investment of

substantial resources and time in transactions that are not consummated; our ability to

successfully integrate or operate acquisitions; the potential impact on us and our tenants,

operators, and borrowers from litigation matters, including rising liability and insurance costs;

environmental compliance costs and liabilities associated with our real estate investments;

ESG and sustainability commitments and requirements, as well as stakeholder expectations;

epidemics, pandemics, or other infectious diseases, including Covid, and health and safety

measures intended to reduce their spread; human capital risks, including the loss or limited

availability of our key personnel; our reliance on information technology systems and the

possibility of a cybersecurity incident or cybersecurity threat affect our information systems

or the information systems of our tenants, operators or borrowers; volatility, disruption, or

uncertainty in the financial markets; increased borrowing costs, including due to rising

interest rates; cash available for distribution to stockholders and our ability to make dividend

distributions at expected levels; the availability of external capital on acceptable terms or at

all, including due to rising interest rates, changes in our credit ratings and the value of our

common stock, bank failures or other events affecting financial institutions; our ability to

manage our indebtedness level and covenants in and changes to the terms of such

indebtedness; the failure of our tenants, operators, and borrowers to comply with federal,

state, and local laws and regulations, including resident health and safety requirements, as

well as licensure, certification, and inspection requirements; required regulatory approvals to

transfer our senior housing properties; compliance with the Americans with Disabilities Act

and fire, safety, and other regulations; laws or regulations prohibiting eviction of our tenants;

the requirements of, or changes to, governmental reimbursement programs such as

Medicare or Medicaid; legislation to address federal government operations and

administrative decisions affecting the Centers for Medicare and Medicaid Services; our

participation in the CARES Act Provider Relief Fund and other Covid-related stimulus and

relief programs; our ability to maintain our qualification as a REIT; our taxable REIT

subsidiaries being subject to corporate level tax; tax imposed on any net income from

; changes to U.S. federal income tax laws, and potential deferred

and contingent tax liabilities from corporate acquisitions; calculating non-REIT tax earnings

and profits distributions; ownership limits in our charter that restrict ownership in our stock;

provisions of Maryland law and our charter that could prevent a transaction that may

otherwise be in the interest of our stockholders; conflicts of interest between the interests of

our stockholders and the interests of holders of Healthpeak OP common units; provisions in

the operating agreement of Healthpeak OP and other agreements that may delay or prevent

unsolicited acquisitions and other transactions; our status as a holding company of

Healthpeak OP; and other risks and uncertainties described from time to time in our

Securities and Exchange Commission filings. Except as required by law, we do not

undertake, and hereby disclaim, any obligation to update any forward-looking statements,

which speak only as of the date on which they are made.

Market and Industry Data

This presentation also includes market and industry data that the Company has obtained

from market research, publicly available information and industry publications. The accuracy

and completeness of such information are not guaranteed. Such data is often based on

industry surveys and experience in the industry. Similarly, although Healthpeak

believes that the surveys and market research that others have performed are reliable, such

surveys and market research are subject to assumptions, estimates and other uncertainties

and Healthpeak has not independently verified this information.

Non-GAAP Financial Measures

This presentation contains certain supplemental non-GAAP financial measures. While the

Company believes that non-GAAP financial measures are helpful in evaluating its operating

performance, the use of non-GAAP financial measures in this presentation should not be

considered in isolation from, or as an alternative for, a measure of financial or operating

performance as defined by GAAP. We caution you that there are inherent limitations

associated with the use of each of these supplemental non-GAAP financial measures as an

analytical tool. Additionally, the computation of non-GAAP financial measures

may not be comparable to those reported by other REITs. You can find reconciliations of the

non-GAAP financial measures to the most directly comparable GAAP financial measures in

the fourth quarter 2023 Discussion and Reconciliation of Non-GAAP Financial Measures

available on our website at http://ir.healthpeak.com/quarterly-results.

2Investor Presentation March 2024

Executive Summary – Continued Strong Execution

3

▪ AFFO of $1.53 per share; +5 pennies better than original guidance

▪ FFO as Adjusted of $1.78 per share; +5 pennies better than original guidance

▪ Same-store growth of 4.8%; +130 basis points better than original guidance

▪ Near-record leasing volume with ~5.1 million square feet of executions across Outpatient Medical and Lab

Fortress

Balance Sheet

2024

Outlook

(1)

▪ 5.2x Net Debt to EBITDA

(1)

and ~$3 billion of liquidity

▪ New 5-year, $750 million term loan swapped to a fixed rate of 4.5%

Recent

Updates

2023

Performance

(1)

▪ Merger with Physicians Realty Trust closed on March 1

st

th

o $40 million of year-one merger synergies included in 2024 Outlook

o Completed property management internalization in four markets to date with an additional five markets scheduled by the end of the second quarter

▪ Received $69 million of proceeds from repayment of seller financing loans in mid-February and under contract on ~$40 million of outpatient dispositions;

continue to pursue less-core property dispositions

▪ AFFO of $1.50 - $1.56 per share; in-line with consensus estimates

▪ FFO as Adjusted of $1.73 - $1.79 per share; includes 3 penny headwind from non-cash merger-related debt mark-to-market

▪ Same-store growth of 2.25% - 3.75%

Investor Presentation March 2024

2025+

Upside

▪ ~$60 million cash NOI

(1)

upside opportunity from temporary downtime at trophy Lab campuses (Vantage, Portside, and Gateway / Directors) and

additional ~$20 million of incremental merger synergies above the $40 million year-one target

▪ Accretive stock buybacks with excess cash including proceeds from less-core property sales and / or seller-financing loan repayments

1) Reconciliations, definitions, and important discussions regarding the usefulness and limitations of the non-GAAP financial measu-

in this presentation can be found in the fourth quarter 2023 Discussion and Reconciliation of Non-GAAP Financial Measures at http://ir.healthpeak.com/quarterly-results-

Total Portfolio Same-of 12/31/23; there is no material change expected in Net Debt to

Adjusted EBITDAre following the merger with Physicians Realty Trust completed on 3/1/2024. The 2024 Outlook ranges provide a framework for metrics of Healthpeak following the merger with

Physicians Realty Trust. We expect to finalize 2024 guidance in late April once 1Q books are closed and GAAP merger adjustments are finalized.

Why Healthpeak

4

Compelling Total Return

Opportunity

3% cash same

-store NOI growth, opportunity for ~$60 million of cash NOI upside across three lab campuses

and $20 million of additional merger synergies, a well

-covered dividend currently yielding ~7.2%, and a stock

price currently trading ~30% below consensus NAV creates a compelling total return opportunity

(1)

Structural Demand

Drivers

Portfolio benefits from continued scientific discovery, an aging population, and the trend toward lower

-cost

outpatient care delivery

Portfolio Quality

Critical mass of purpose

-built lab campuses in the three most important clusters and a high-quality outpatient

medical portfolio leased to leading health systems and specialty physicians

Competitive Advantage

Decades of operational expertise and relationships drive internal and external growth opportunities

Fortress Balance Sheet

5.2x

Net Debt to EBITDA

(2)

, limited floating rate debt, and no material 2024 debt maturities

Sustainable and

Responsible Business

Sustainability embedded into our business model and operating plan; committed to strong governance

1) 3% same-store growth represents the mid--store Outlook, See page 9 for details on estimated NOI u

and a share price of $16.75 as of 2/29/24. Consensus NAV per share of $24.77 as of 2/29/24 per CapIQ. Reconciliations, definitions, and important discussions regarding the usefulness and limitations of

the non--nd in the fourth quarter 2023 Discussion and Reconciliation of Non-

GAAP Financial Measures located at http://ir.healthpeak.com/quarterly---Store Cash (Adjusted) NOI growth.

2) Net Debt to Adjusted EBITDAre following the merger with Physicians

Realty Trust completed on 3/1/24.

Investor Presentation March 2024

Strategic Merger Benefits

The combination of Healthpeak and Physicians Realty Trust accelerates key strategic goals

5

Create Best

-In-Class Platform

Combined senior team has 200+ years of outpatient medical operating experience

Drive Internal Growth

Favorable supply / demand fundamentals are producing at or near all

-time highs for outpatient

medical same

-store, retention, and releasing spreads

Grow Earnings

Increases 2024 AFFO by 5 pennies per share (+3.4% versus stand

-alone Healthpeak)

Lower Cap

-Ex

Legacy Physicians Realty Trust portfolio comprised of younger assets with longer WALT and higher

percentage of investment grade tenants, resulting in lower cap

-ex than industry averages; earnings

and same

-store are important metrics, but cash flow drives IRR

Maintain Strong Balance Sheet

Improves leverage and extends weighted average maturity

Improve G&A Efficiency

Healthpeak G&A essentially flat despite adding ~$5 billion of assets

Expand Growth Relationships

No company better networked in the outpatient medical sector; relationships create outsized internal

and external growth opportunities

Investor Presentation March 2024

Strategic Goal

Merger Benefit

Delivering Earnings Results & Exceeding Expectations

6

FFO as Adjusted

Same-Store

Growth

Original 2023 Guidance

(1)

Actual 2023 Results

(1)

Midpoint Variance

$1.73 $1.78 + $0.05

$1.48 $1.53 + $0.05

3.5% 4.8% + 130 bps

1) -GAAP financial measures can be found in the Discussion and

Reconciliation of Non-GAAP Financial Measures for the fourth quarter 2022 (for Original 2023 Guidance) and the fourth quarter 2023 (for Actual 2023 Results), in each case at

http://ir.healthpeak.com/quarterly-results.

AFFO

Investor Presentation March 2024

Strong track record for exceeding guidance

2020-2022 Avg. 2023

Note: Lease executions for legacy Healthpeak portfolio only.

2023 Lease Executions Above the 3-Year Average

7Investor Presentation March 2024

+6%

4.8M SF

5.1M SF

Record or near-record lease executions,

tenant retention, and lease spreads led to

year-end same-store occupancy of ~92%,

with +4% cash renewal spreads

Outpatient Medical

Lab

~90% of lease executions in our three core

markets were with existing tenants,

demonstrating the importance of scale and

relationships to drive leasing success

Continued growth in outpatient demand and strong lab relationships drove above-trend leasing volumes

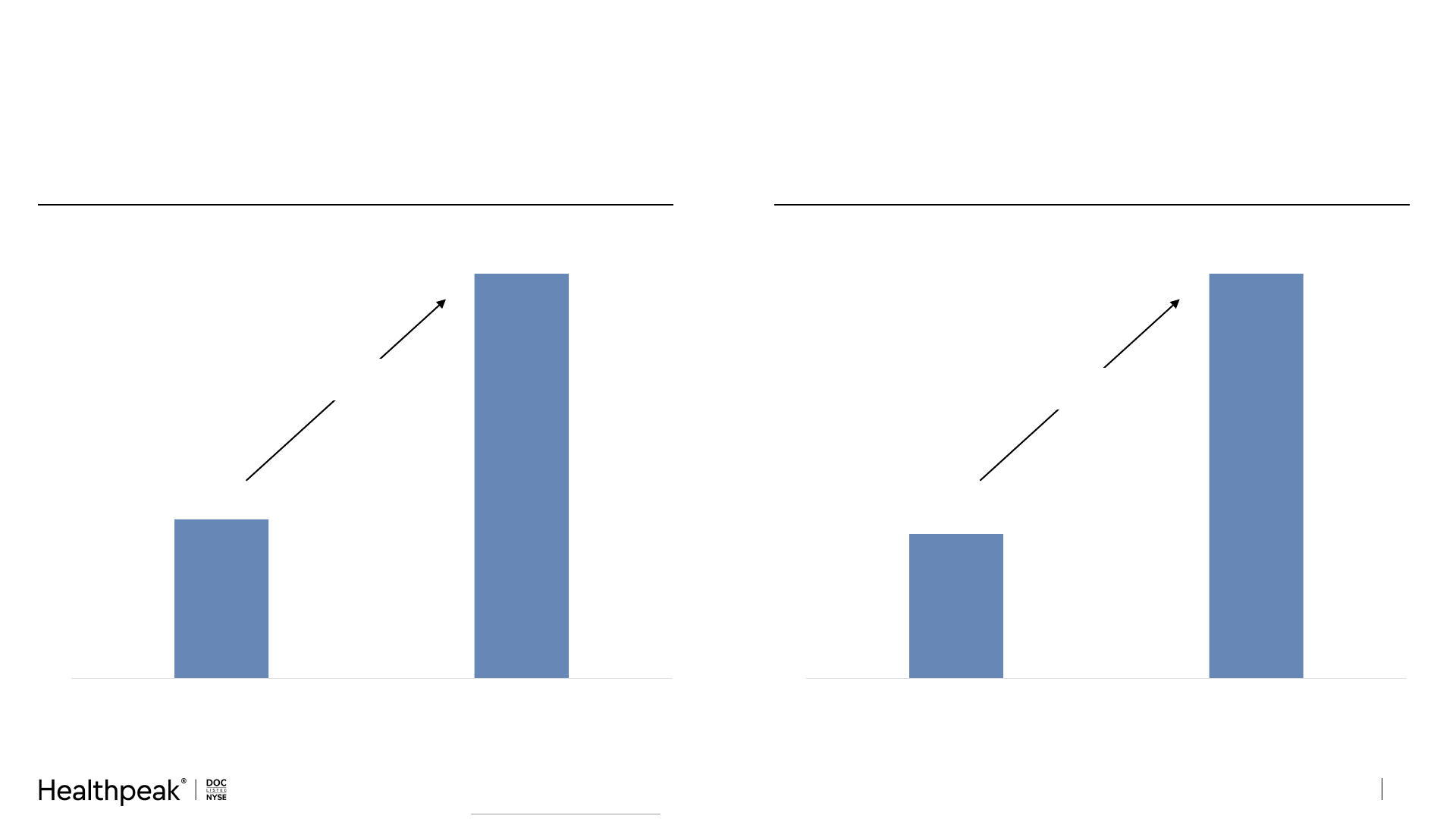

Double Digit Earnings Growth Over the Past Two Years

8

FFO as Adjusted per Share

(1)

AFFO per Share

(1)

$1.61

$1.78

2021 2023

$1.35

$1.53

2021 2023

+11%

+13%

Investor Presentation March 2024

Earnings growth driven by development earn-in, property performance, and a more efficient G&A structure

Note: Represents earnings growth for legacy Healthpeak only.

1) Reconciliations, definitions, and important discussions regarding the usefulness and limitations of the non-GAAP financial measures can be found in the fourth quarter 2023 Discussion and Reconciliation

of Non-GAAP Financial Measures located at http://ir.healthpeak.com/quarterly-results.

.

Significant Potential Growth Opportunity

9

Vantage Phase I

Development

(1)

Gateway / Directors

Dev & Redev

(1)

Portside

Redevelopment

(1)

Additional Merger

Synergies

(2)

+$15M

+$20M

+$25M

+$20M

2025+ Upside Opportunity

+$80M

1) Estimated stabilized cash NOI is based on a mid-point of current market rents. Subject to change based on market conditions.

2) Represents incremental merger-

Investor Presentation March 2024

~$60 million of cash NOI upside and ~$20 million of additional merger synergies that are not included in our 2024

earnings Outlook; majority of capital needed to achieve upside already incurred or included in 2024 forecast

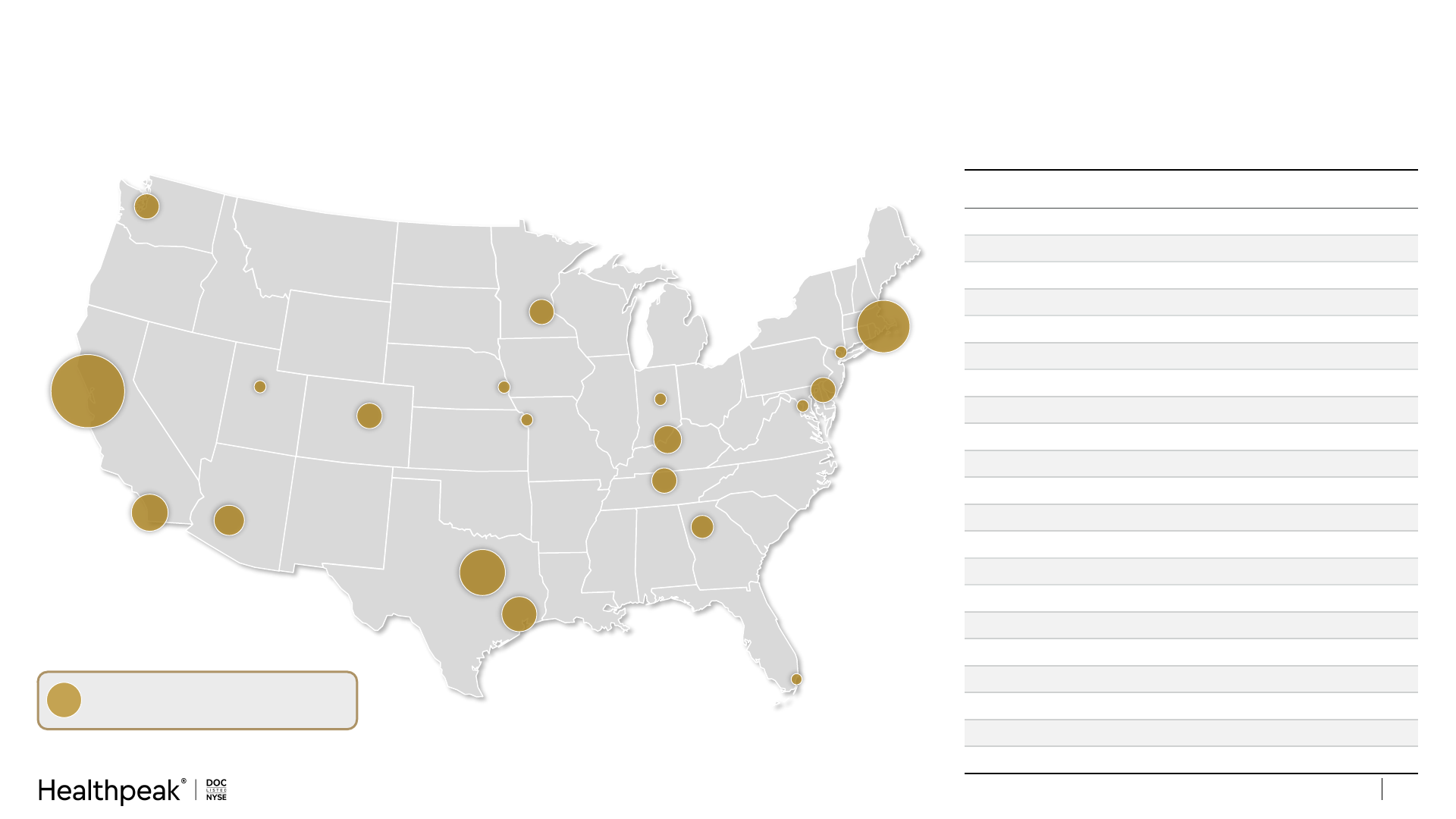

National Scale, Local Competitive Advantage, Attractive Diversification

10

13 markets with footprints of 1 million square feet or more to help drive local competitive advantage

Bay Area /

South San Francisco

25%

Boston

10%

Dallas

8%

San Diego

6%

Houston

4%

Phoenix

3%

Louisville

3%

Nashville

3%

Seattle

2%

Atlanta

2%

Denver

2%

Minneapolis

2%

Indianapolis

1%

Philadelphia

2%

New York

1%

Salt Lake City

1%

Miami

1%

Washington, DC

1%

Omaha

1%

Kansa City

1%

Rank

Market

Square Feet

(M)

% of ABR

(1)

1

Bay Area (S. SF), CA

(2)

6.3 25%

2

Boston, MA 2.8 10%

3

Dallas, TX 4.6 8%

4

San Diego, CA 3.0 6%

5

Houston, TX 3.6 4%

6

Nashville, TN 1.8 3%

7

Phoenix, AZ 1.8 3%

8

Louisville, KY 1.9 3%

9

Denver, CO 1.2 2%

10

Seattle, WA 1.1 2%

11

Atlanta, GA 1.2 2%

12

Minneapolis, MN 1.0 2%

13

Philadelphia, PA 1.3 2%

14

New York, NY 0.8 1%

15

Indianapolis, IN 0.8 1%

16

Salt Lake City, UT 0.8 1%

17

Miami, FL 0.6 1%

18

Washington, DC 0.5 1%

19

Kansas City, MO 0.5 1%

20

Omaha, NE 0.7 1%

Remainder 15.0 21%

Top 20 Outpatient and Lab Markets

Sized in proportion to % of ABR

Investor Presentation March 2024

1) CRC / Senior Housing JV portfolio.

2) Primarily consists of the city of South San Francisco, located 10+ miles south of the central business district of San Francisco, in San Mateo County. Healhpeak does not own any assets in the city or county of San Francisco.

34%

16%

11%

8%

7%

7%

7%

6%

4%

Diversified Tenant Base and Leading Relationships

11

Unmatched roster of leading biopharma, health systems, and physician groups to drive internal and external growth;

only two tenants represent more than 1% of ABR

1) Specialty outpatient services includes tenant types such as non-health system ambulatory surgical centers, cancer treatment and dialysis centers, imaging and radiology, urgent care and sleep labs. Large Cap Biopharma represents companies

with a market cap (as of 12/31/2023) as follows: >$10B; Mid Cap between $10B and $500M; and Small Cap: <$500M.

2) Top 20 Tenants excludes Amgen due to recent lease expirations.

3) urt

portfolio.

Rank

Parent Name Classification

% of ABR

(3)

1

HCA Healthcare Health System 9%

2

CommonSpirit Health Health System 3%

3

Astellas Pharma Large Cap Biopharma 1%

4

McKesson Corporation Health System 1%

5

University of Louisville Health System 1%

6

Ascension Health Health System 1%

7

Tenet Healthcare Health System 1%

8

Northside Hospital Health System 1%

9

Bristol-Myers Squibb Large Cap Biopharma 1%

10

Arcus Biosciences Mid Cap Biopharma 1%

11

Johnson & Johnson Large Cap Biopharma 1%

12

Community Health Systems Health System 1%

13

Memorial Hermann Health System 1%

14

Myriad Genetics Mid Cap Biopharma 1%

15

Norton Healthcare Health System 1%

16

HonorHealth Health System 1%

17

Novo Nordisk Large Cap Biopharma 1%

18

Pfizer Large Cap Biopharma 1%

19

Nkarta Small Cap Biopharma 1%

20

Alphabet (Calico subsidiary) Large Cap Biopharma 1%

Physician Group Practices

Large Cap Biopharma

CCRC / SH

Mid Cap

Biopharma

Small Cap

Biopharma

Private

Biopharma

Other

Tenant Diversification

(1)

Health System

Top 20 Tenants

(2)

Med Device / R&D / University &

Specialty Outpatient Services

$1.7B

Annualized

Base Rent

(3)

Investor Presentation March 2024

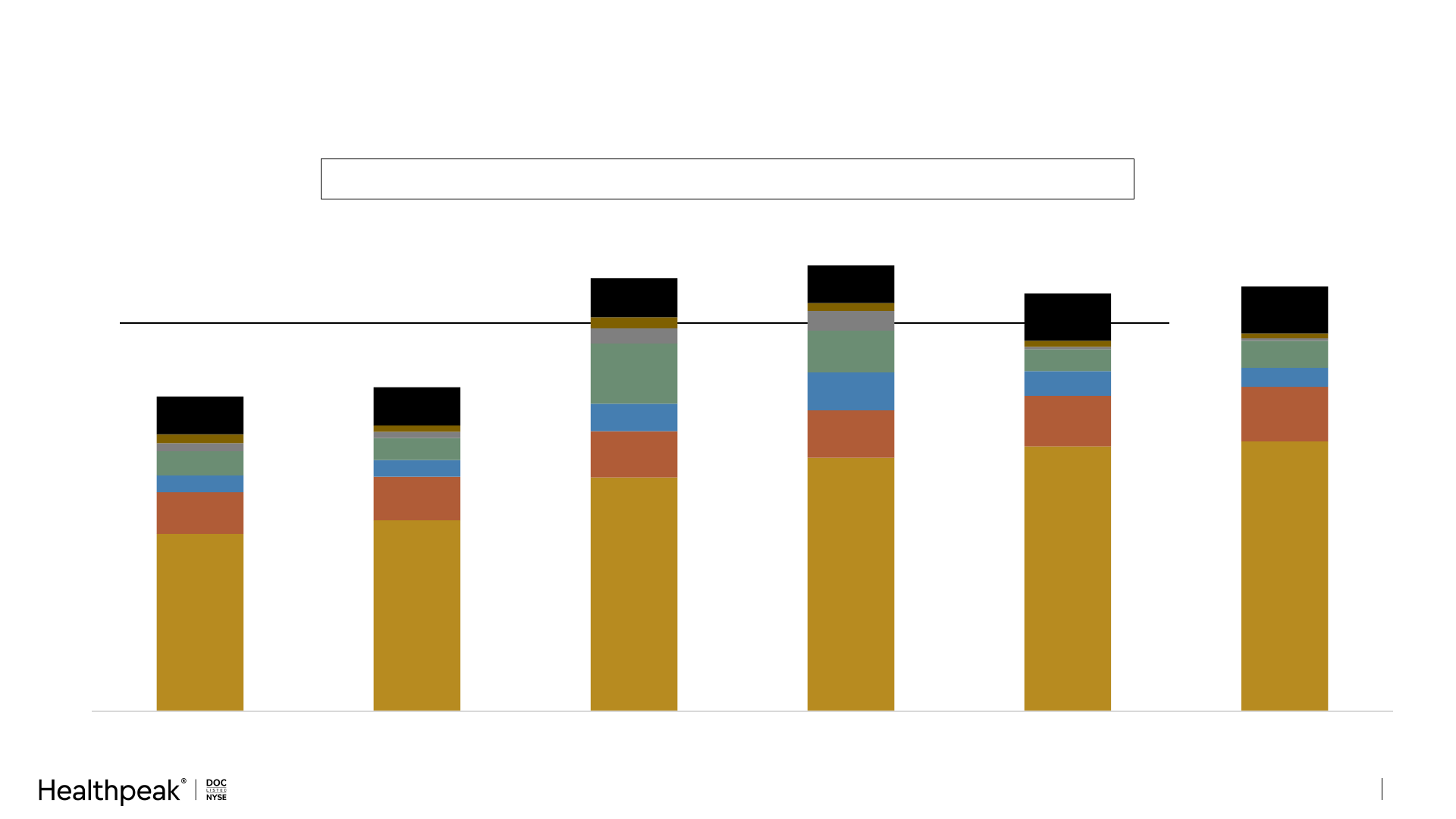

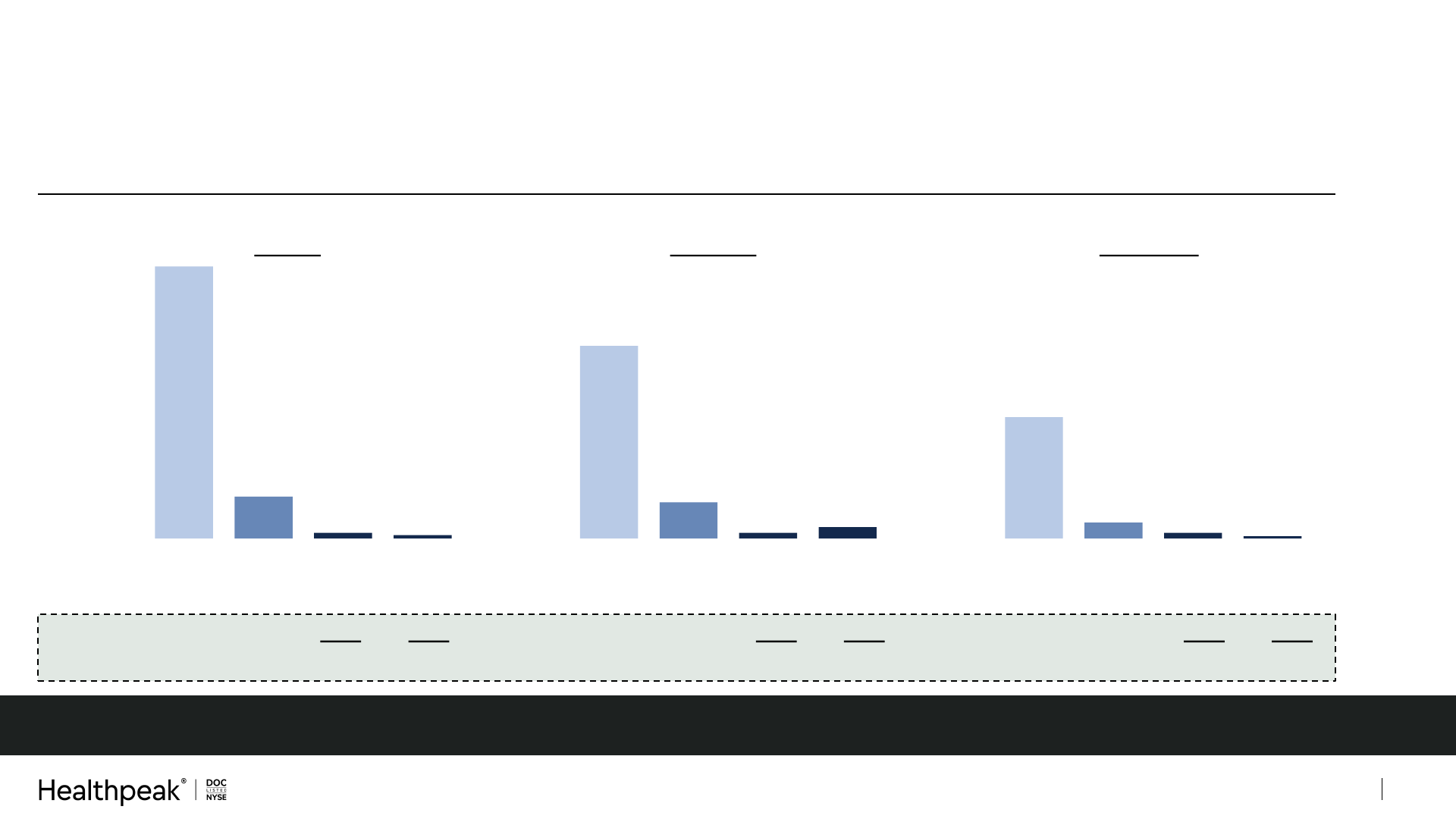

Fortress Balance Sheet

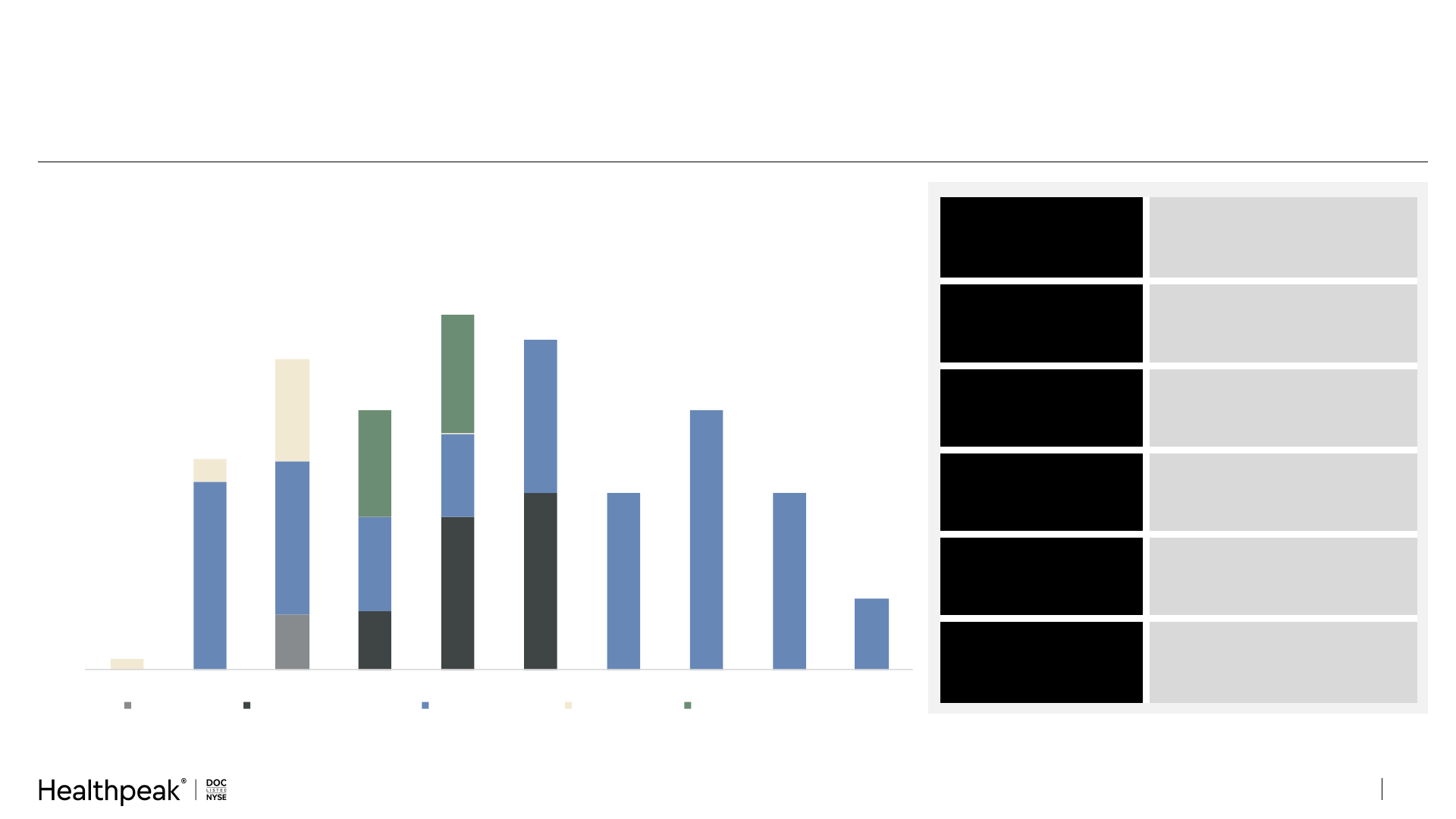

Debt Maturities and Credit Metrics

(1)(2)

($ in billions)

12

1) As of 12/31/23 adjusted to reflect the merger with Physicians Realty Trust, a new $750M unsecured term loan maturing in 2029, re

ing unsecured term loan, unsecured bonds, and mortgage debt.

2) Assumes one-

3) Based on coupon rate and excludes amortization of any discount / premium and deferred financing costs.

4) Includes variable rate loans receivable of $110M.

5) Net Debt to Adjusted EBITDAre following the merger with

Physicians Realty Trust completed on 3/1/2024.

6) ty.

Weighted Average

Interest Rate

(3)

3.8%

Weighted Average

Debt Maturity

(2)

4.9 years

Secured Debt

Percentage

2.3%

Net Floating Rate

Debt Exposure

(4)

2.3%

Net Debt / Adjusted

EBITDA

(5)

5.2x

Liquidity

(6)

~$3B

Strong balance sheet with well-laddered maturities and low floating rate debt exposure

$0.2

$0.3

$0.7

$0.8

$0.8

$0.7

$0.4

$0.4

$0.7

$0.1

$0.4

$0.5

$0.5

$0.0

$0.9

$1.3

$1.2

$1.6

$1.5

$0.8

$1.1

$0.8

$0.3

$-

$0.5

$1.0

$1.5

$2.0

2024 2025 2026 2027 2028 2029 2030 2031 2032 Thereafter

Revolver / CP Unsecured Term Loans Unsecured Bonds Secured Debt Unsecured Green Bonds

Investor Presentation March 2024

Outpatient Medical

Overview

4.6

3.6

1.9

1.8

1.8

1.3

1.2

1.2

1.1

1.0

Dallas, TX

Houston, TX

Louisville, KY

Nashville, TN

Phoenix, AZ

Philadelphia, PA

Denver, CO

Atlanta, GA

Seattle, WA

Minneapolis, MN

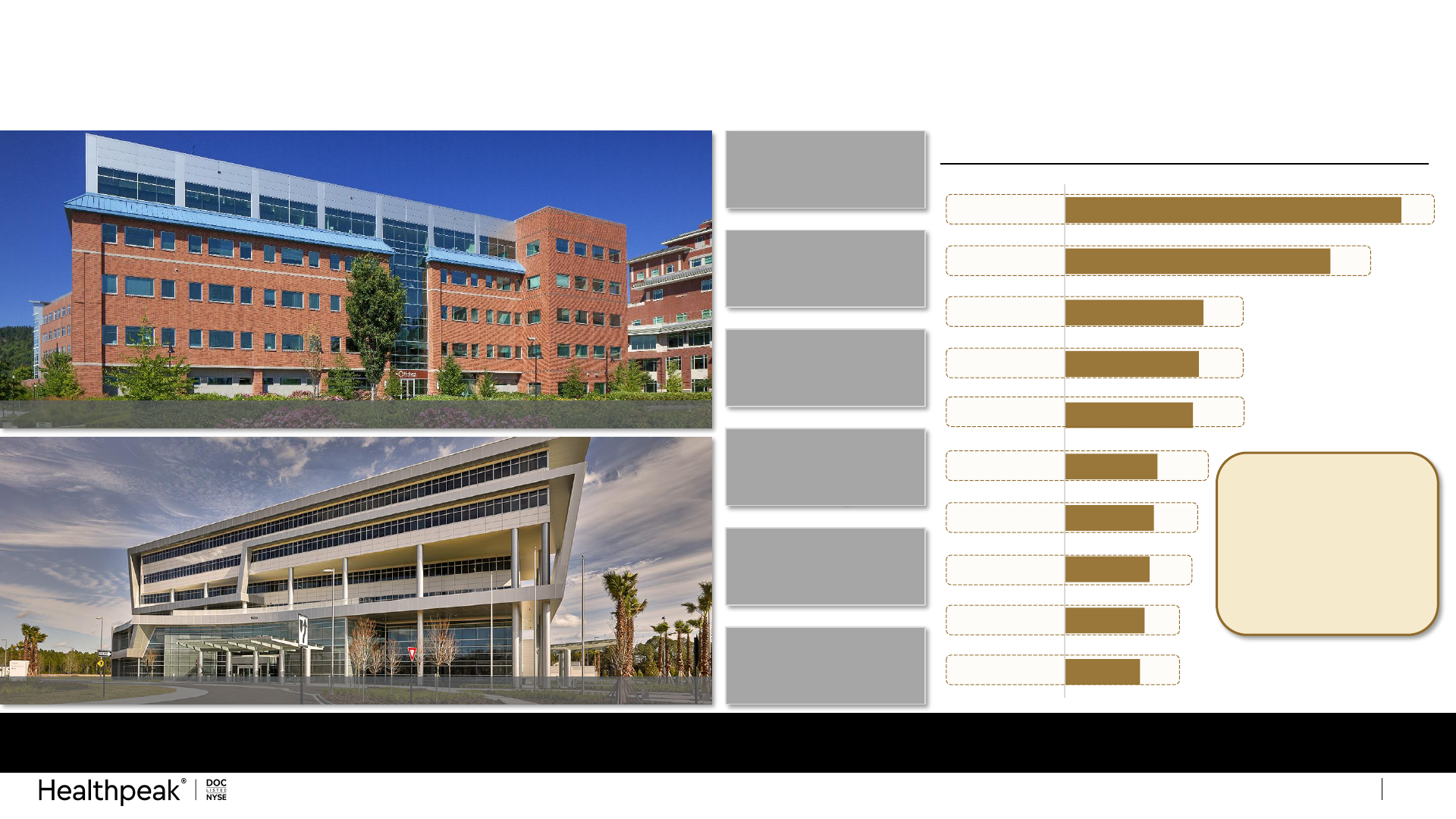

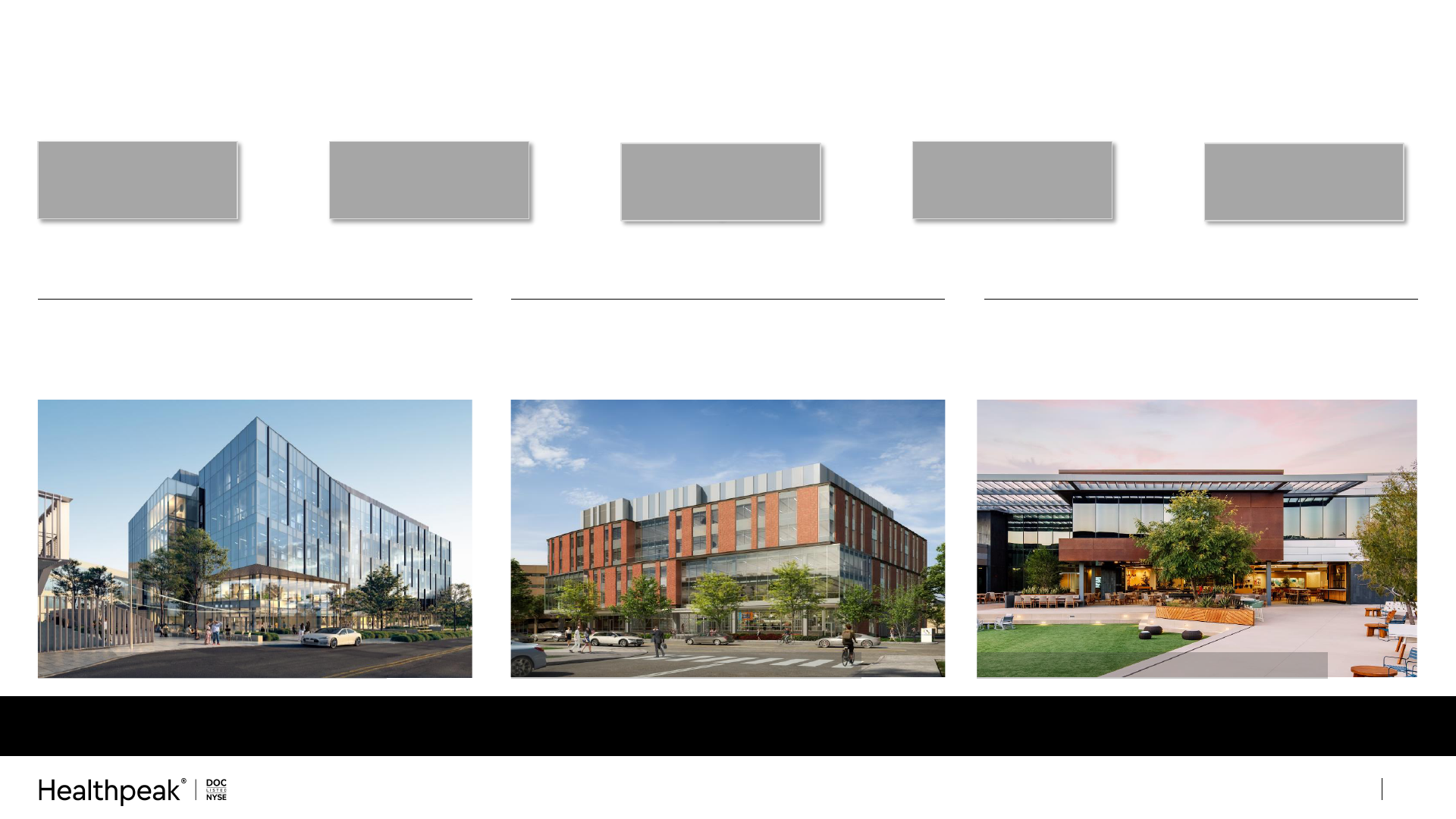

Unmatched Outpatient Medical Platform and Portfolio

14

40M sq. ft. Outpatient Medical portfolio with concentration in high-growth markets and local competitive advantage

UF Health North Medical Building | Jacksonville, FL

Top 10 Healthpeak Outpatient Medical MSAs

(Based on square footage in millions)

95%

On-Campus or Affiliated

~30M+

Annual Patient Visits

10/10

Relationships With Top

10 Health Systems

575

Properties

40M

Sq. Ft.

~60%

Investment Grade

(1)

Considerable opportunity to internalize property management and generate earnings upside

1) Calculated as leased investment grade square footage over total leased square footage. Represents companies with a credit rating -, and Fitch: BBB- or higher. Also includes investment grade quality

tenants without public debt outstanding. Investment grade quality tenants without public debt outstanding represents ~2%.

Northwest Specialty Center | Springfield, OR

Internalized property

management in Phoenix

and Dallas in Q1; targeting

Louisville, Nashville,

Seattle, Chicago, and

Indianapolis during Q2

with additional markets

over time

Investor Presentation March 2024

3.5%

4.7%

2010 - 2019 average 2022 - 2030E average

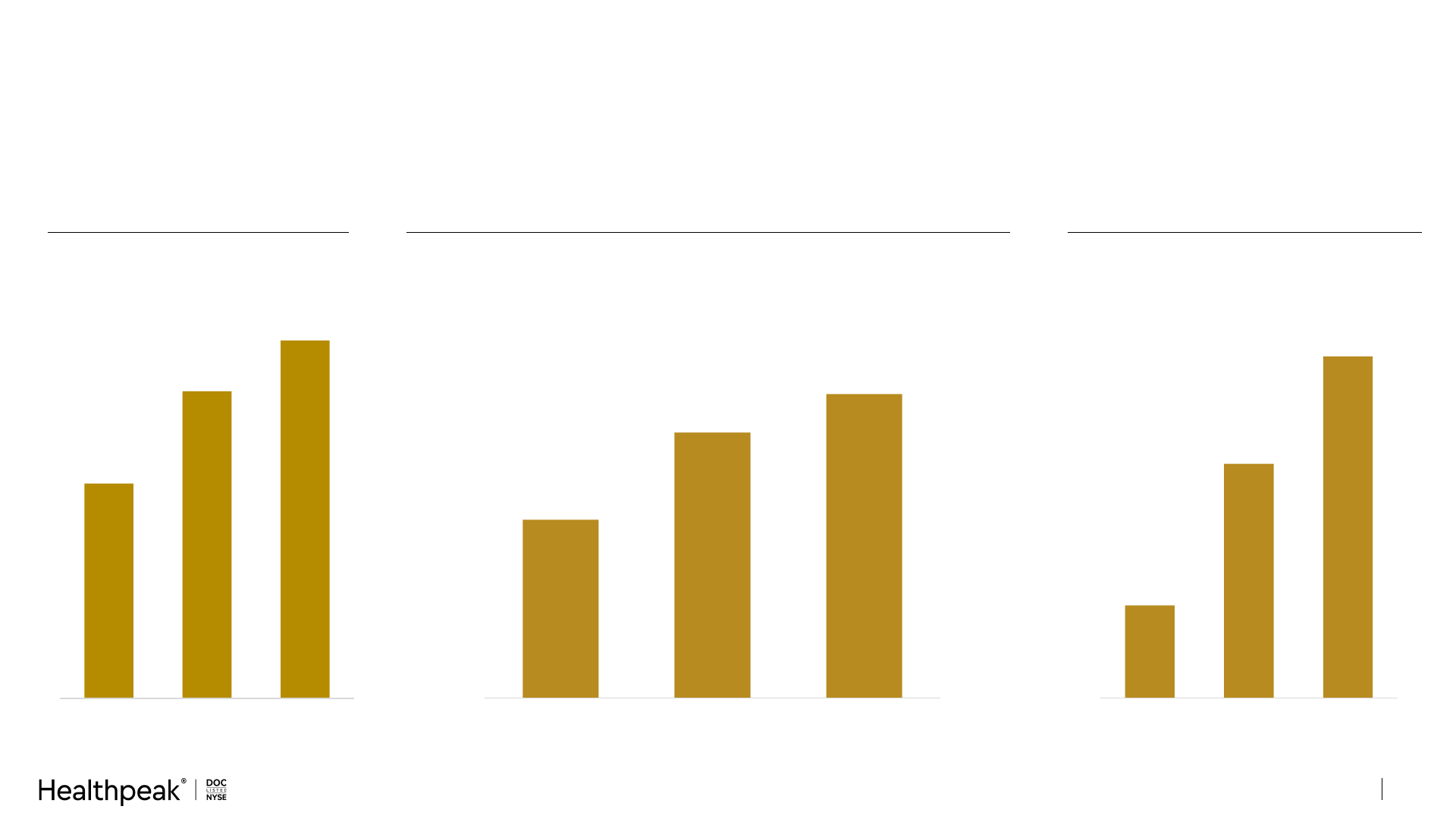

Outpatient Medical Demand Drivers are Stronger Than Ever

15

Aging Senior Population

(US age 65+ in millions)

Average Annual Growth in Health Expenditures

(per capita

(1)

)

Outpatient Visits Growing

(per 1,000 population)

Investor Presentation March 2024

41

59

69

2011 2023 2031E

2,100

2,400

2,850

2010 2022 2032E

The structural trends of an aging population and the growth in healthcare spending support continued growth in lower-

cost outpatient care settings, which should generate long-term demand for our real estate

Sources: Stratodem, CDC, KFF, and Advisory Board estimates.

1) 2020 and 2021 excluded from the averages due to the one-time impact on health expenditures related to COVID.

Average growth in annual spending expected to

accelerate compared to the prior decade

10.4

13.7

2019 2023

14.0

7.9

2019 2023

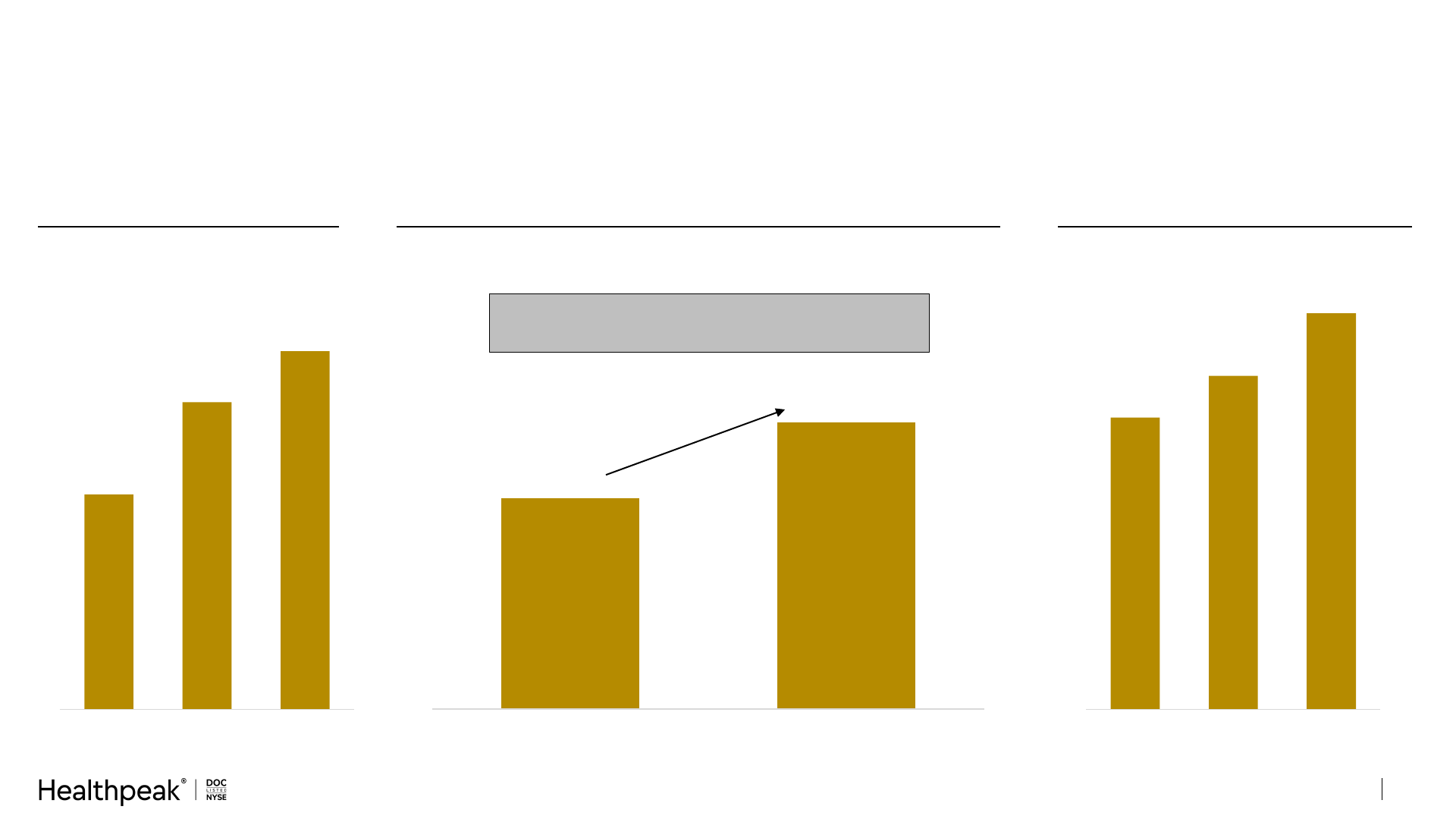

Outpatient Medical Fundamentals Driving Improved Growth

16

Increasing Absorption

(TTM absorption in sq. ft. millions)

Declining Development Starts

(TTM starts in sq. ft. millions)

Sector Occupancy Trending Higher

91.3%

92.6%

2019 2023

Healthpeak’s Rent Mark

-to-Market Increasing

(1)

(Cash lease spreads on renewals)

Sources: Absorption, development start and occupancy data from Revista.

1) Includes both Healthpeak and Physicians Realty Trust combined outpatient portfolios.

2) Average same-

Investor Presentation March 2024

Up ~30%

Down ~40%

Up 130 bps

Up 200 bps

Demand exceeds supply and is generating increased occupancy and rent growth, which we expect to continue

Healthpeak’s Outpatient Same-Store Growth

(2)

2.5%

3.5%

2013 - 2020 Average 2021 - 2023 Average

Up 100 bps

2%

4%

2018 - 2022 Average 2023

Strong Tenant Credit and Importance of Relationships

17

Space in Our Portfolio Leased by Health Systems Has More Than

Doubled

1) 2023 is based on Healthpeak and Physicians Realty Trust combined outpatient portfolio.

2) Healthpeak and Physicians Realty Trust combined outpatient portfolio.

3) U.S. physician breakdown from AAMC, 2022 Physician Specialty Data Book.

Focus on Specialty Physicians and Services Limits

Competition from Retail Clinics or Telemedicine

Types of Specialties

Healthpeak

(2)

National

Benchmark

(3)

Orthopedics 11% 4%

Oncology 10% 3%

Ambulatory Surgery Center 9% N/A

Obstetrics / Gynecology 7% 5%

Cardiovascular 6% 4%

General / Specialty Surgery 6% 4%

Imaging / Radiology 6% 3%

Ophthalmology 3% 2%

Neurology 3% 2%

Other 23% 40%

Total Specialties

84% 67%

Primary Care

16% 33%

2003 2023

(1)

25% 66%

Health Systems Other Physicians & Outpatient Services

Investor Presentation March 2024

Health systems have significantly expanded their outpatient footprint as healthcare delivery has shifted to an

outpatient model; the growth in outpatient is likely to continue and no company is better positioned to support this

growth than Healthpeak

2013

45% 65%25%

Lab

Overview

Concentrated Lab Clusters Across the Leading Markets

19

Well-located portfolio of amenity-rich spaces for R&D and collaboration

Embedded long-term growth opportunities from well-located, developable land sites across leading lab submarkets

97%

Occupied

Operating Portfolio

~5M+ Sq. Ft.

Future Development

Densification Potential

85%

ABR from Campuses

over 400,000 Sq. Ft.

146

Properties

12M

Lab Sq. Ft.

Investor Presentation March 2024

Nexus on Grand | South San Francisco, CA 101 CambridgePark Drive | Cambridge, MA

Bay Area

Preeminent lab real estate owner in

South San Francisco

Boston

Cambridge and Lexington focused portfolio

with a pathway to significant future growth

San Diego

Strategically positioned in Torrey Pines and

Sorrento Mesa

The Boardwalk | Torrey Pines, CA

Aging Senior Population

(US age 65+ in millions)

Positive Long-Term Demand Drivers for Lab

Sources: Stratodem, Evaluate Pharma, Precedence Research, BLS, CMS.gov, Healthpayer Intelligence.

20

Increasing Drugs Approvals

(New Drugs Approved by the FDA)

Growing Global Drug Demand

(Global Pharmaceutical Drug Sales in $B)

Investor Presentation March 2024

41

59

69

2011 2023 2031E

$741

$1,880

$2,740

2011 2023 2031E

143

213

244

2009-2013 2014-2018 2019-2023

With an aging population and accelerating scientific discovery and drug approvals, we expect a long-term virtuous

cycle that will support ongoing demand for our real estate

192

207

254

275

287

293

45

47

50

51

55

59

18

18

30

41

26

22

26

24

65

46

24

29

16

21

41

41

42

41

51

51

$341B

$351B

$469B

$483B

$453B

$461B

$0B

$100B

$200B

$300B

$400B

$500B

$600B

2018 2019 2020 2021 2022 2023

2018 – 2022 Average: ~$420B

Supportive Biopharma Capital Raising and R&D Trends

Source: DealForma, S&P Global, NIH.gov, Giving USA

1) Only includes partnership funding with disclosed financial details; majority of partnership financial commitment details are not publicly available.

2) 2023 reflects 2022 data as 2023 data is still pending.

3) 2023 Global Biopharma R&D represents annualized 3Q23 YTD data due to 4Q23 data pending.

21

Global Biopharma R&D NIH/NSF VC SEO IPO Partnerships

(1)

Healthcare Philanthropy

Investor Presentation March 2024

The lab industry benefits from diversified funding sources; 2023 funding was above the 2018-2022 average

(2)

(3)

Biotech Public Equity Funding Up Significantly YoY

Select Healthpeak Tenant Capital Raise

Activity

Recent Lab Capital Raising Trends Improving Tenant Credit

22

$0

$15

$12B | 68 deals

Sources: Baird Weekly Biotech Update as of 2/26/24 and public disclosures.

February 2024

VC Funding

$120M

January 2024

$66M upfront

partnership with

January 2024

$125M

Follow-On

Equity Offering

January 2024

$100M

Follow-On

Equity Offering

January 2024

$2.2B acquisition by

February 2024

$287.5M

Follow-On

Equity Offering

Jan to Feb 2023

$4B | 36 deals

January 2024

$100M upfront

partnership with

February 2024

$127.5M

Follow-On

Equity Offering

Investor Presentation March 2024

The positive momentum in biotech valuations has led to an active funding market to start 2024; expected to contribute

towards improved levels of space demand over next 6-12 months

February 2024

$500M

Follow-On

Equity Offering

Jan to Feb 2024

Up 200%

Competitive New Supply

Healthpeak’s near-term lease roll is modest; speculative development starts have fallen to near zero which should

provide a multi-year window beyond ’25 of limited deliveries allowing for further market stabilization and recovery

2024

2025

0.0%

1.0%

23

Boston Bay Area San Diego

Healthpeak Expirations

(% of total lab sq. ft.)

2024

2025

3.0%

(2)

4.3%

2024

2025

0.4%

4.9%

Lab Inventory and

New Supply by Market

(1)

Sorted by market inventory (sq.

ft. in millions)

1) -Cambridge, San Francisco Bay Area, and San Diego. Under Construction includes new development, conversions,

speculative and build-to-suit projects. 2024 & 2025 Unleased Competitive Supply based on Healthpeak assessment of submarket, building quality, sponsorship and other qualitative factors to determine the

relative competitive profile of each development. A portion of the Under Construction pipeline could be partially competitive, but not directly competitive, based on the factors mentioned above.

2) Excludes 250,000 sq. ft. planned to enter redevelopment upon lease expiration on the Portside and Pointe Grand campuses.

Headline new supply numbers include projects that we believe are not directly competitive due to a combination of submarket locations,

inferior building design & capability, and / or sponsorship by developers with limited credibility and footprint

Total

Market

Inventory

Total

Under

Construction

Unleased Competitive

Supply

2024 2025

Total

Market

Inventory

Total

Under

Construction

Unleased Competitive

Supply

2024 2025

Total

Market

Inventory

Total

Under

Construction

Unleased Competitive

Supply

2024 2025

Investor Presentation March 2024

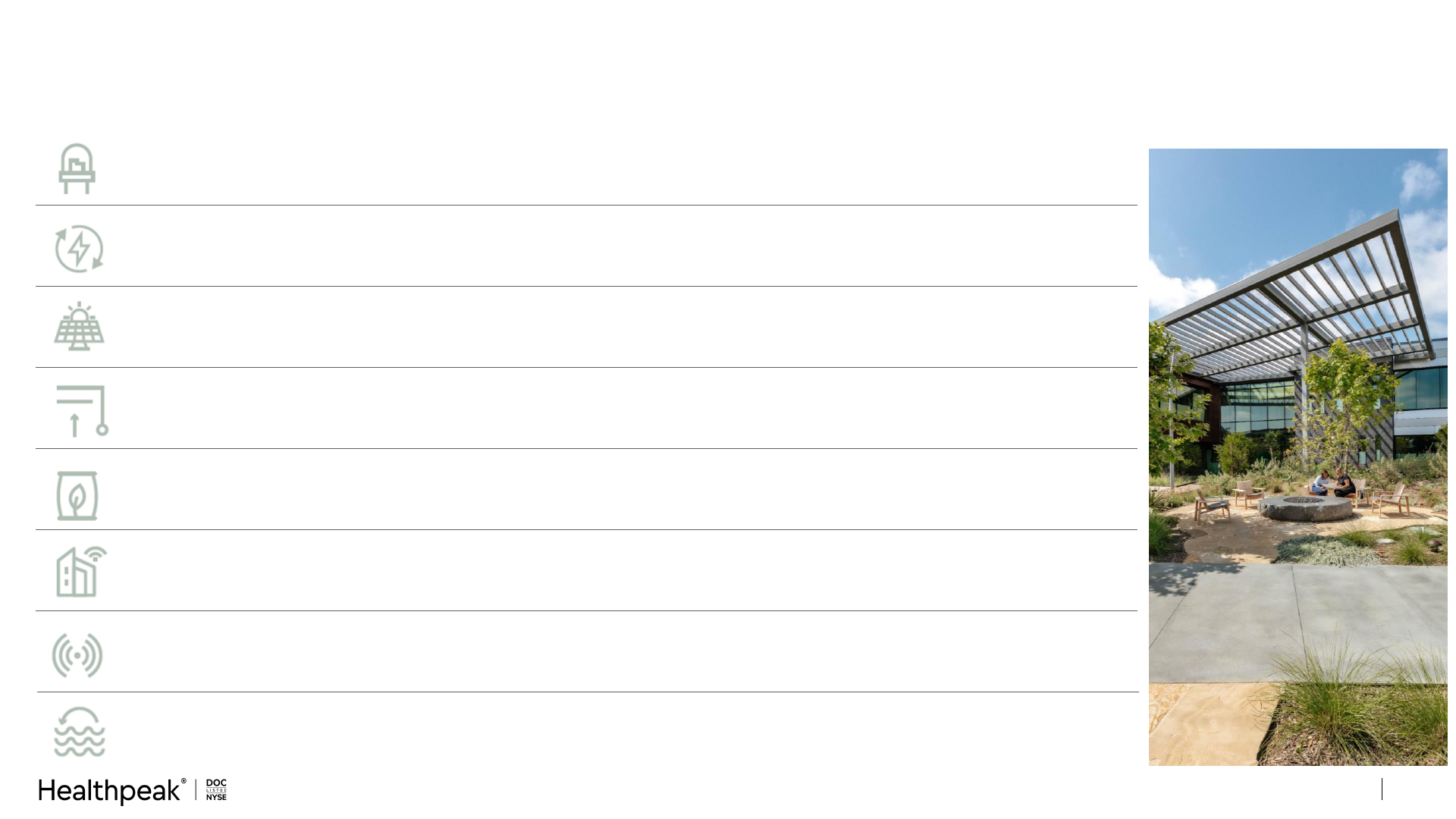

Sustainable

and

Responsible Business

Sustainability in Action

Improving our portfolio through sustainability initiatives

25

LED Lighting

Energy-Efficient

HVAC Systems

Renewable

Energy

Window Film &

Smart Windows

Recycling &

Composting

Occupancy

Sensors

Smart Building

Technology

Water

Conservation

Optimize energy efficiency by using LED lighting in new construction and through retrofits

Implement upgrades and replacements to help drive energy savings, including boiler retrofits,

compressor replacements, adding variable frequency drives and whole system replacements

Utilize on-site renewables such as solar and off-site renewables such as wind power when

feasible and procure offsite renewable energy through renewable energy certificates

Install energy-saving window films and use "smart" view glass windows to automatically control

temperature and glare

Work with property managers and tenants to implement best practices for waste management

and landfill diversion, including recycling and composting

Install occupancy sensors in our properties to reduce energy usage

Use self-regulating electrical systems that adjust automatically based on feedback from the

surrounding environment, increasing power grid efficiency and cost-effectiveness

Maximize water savings through drought-tolerant landscaping, drip irrigation, smart controllers,

low-flow sprinkler heads, efficient plumbing fixtures and condensate recovery systems

Investor Presentation March 2024

Environmental

Social

Governance

Governance Intelligence and

IR Magazine

Winner – Best Proxy

Statement (Mid Cap)

Finalist – Best ESG

Reporting (Mid Cap)

Fortune Best Workplaces in Real Estate

2 Consecutive Years

CDP Leadership Band

11 Consecutive Years

S&P Global

Dow Jones Sustainability World Index

4 Times

Dow Jones Sustainability N. America Index

11 Consecutive Years

Sustainability Yearbook

9 Consecutive Years

Newsweek

Responsible Companies

5 Times

Bloomberg Gender-Equality Index

4 Consecutive Years

20/20 Women on Boards

Board Diversity Recognition

5 Times

MSCI Rating

AA

Recognized Leader in Corporate Responsibility

GRESB Green Star Rating

12

Consecutive Years

FTSE4Good Index Series

12

Consecutive Years

Top / Best Place to Work Recognitions

Orange County, Milwaukee and Tennessee

Great Place to Work Certified

4 Consecutive Years

ISS ESG Corporate Rating

Prime

Top 10% QualityScore

Score of “1”

ENERGY STAR Partner of the Year

3 Times

Green Lease Leader

Platinum

Modern Healthcare Best Places to Work

3 Times

Reflects recognitions of each legacy company prior to the completion of the merger.

26Investor Presentation March 2024